Economic Forecasts

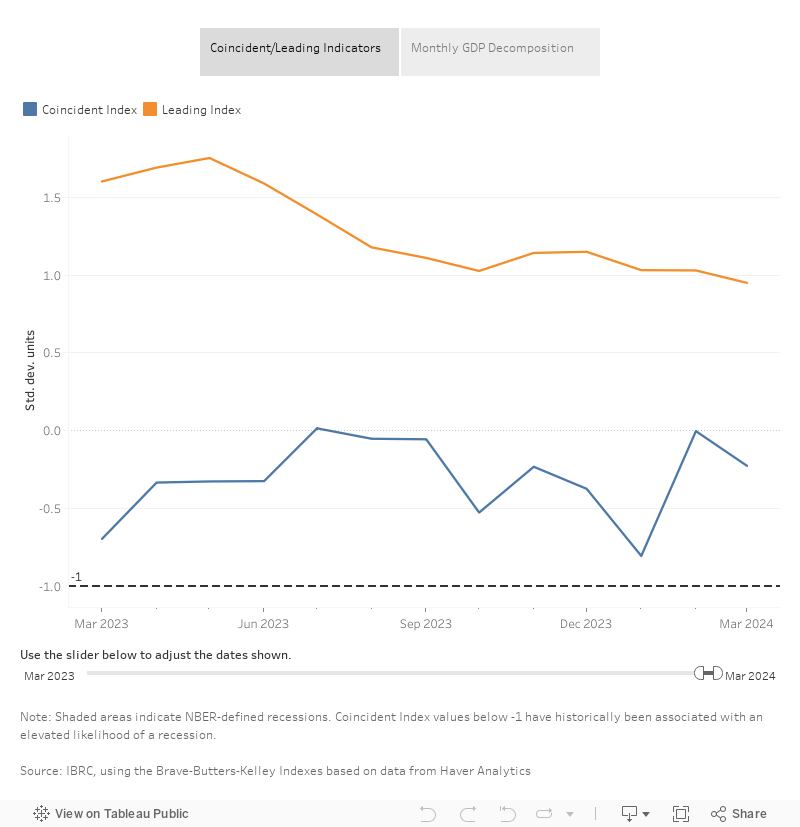

Brave-Butters-Kelley Indexes (BBKI)

The Brave-Butters-Kelley Indexes (BBKI) provide a timely and accurate depiction of the state of economic activity for the U.S. and can be utilized to gauge the future trajectory of economic activity. These data exhibit predictive power for business cycle fluctuations and summarize the information in an unbalanced panel of 490 macroeconomic time series extending back to 1960.

- View current data and analysis

- Tracking the economy with the Brave-Butters-Kelley Indexes (Indiana Business Review, Fall 2022)

Forecasts from the Center for Econometric Model Research

The Center for Econometric Model Research at Indiana University produces U.S. forecasts each month. Indiana, metro area and long-range forecasts are produced on a quarterly basis. The current forecast summaries are available below.

Futurecast: Business Outlook Program

Each fall since 1972, a group of IU faculty gathers at the Kelley School of Business to consider the economic outlook for the coming year. They then present their national, state and local forecasts in various Indiana cities each year.

Archive

- The Federal Reserve Bank of Philadelphia produced leading indexes for each of the 50 states each month, which predicted the six-month growth rate of the state's coincident index, but has suspended the release of the state leading indexes indefinitely.